Adapting to Rising Insurance Prices in Wildfire Zones in the American West

Adapting to Rising Insurance Prices in Wildfire Zones in the American West

A coin has two sides. You can flip a “heads” or a “tails”. Homeowners often seek to flip “one sided” coins. Over the last 25 years, home prices have soared in California and owners proudly want to pocket their huge capital gains.

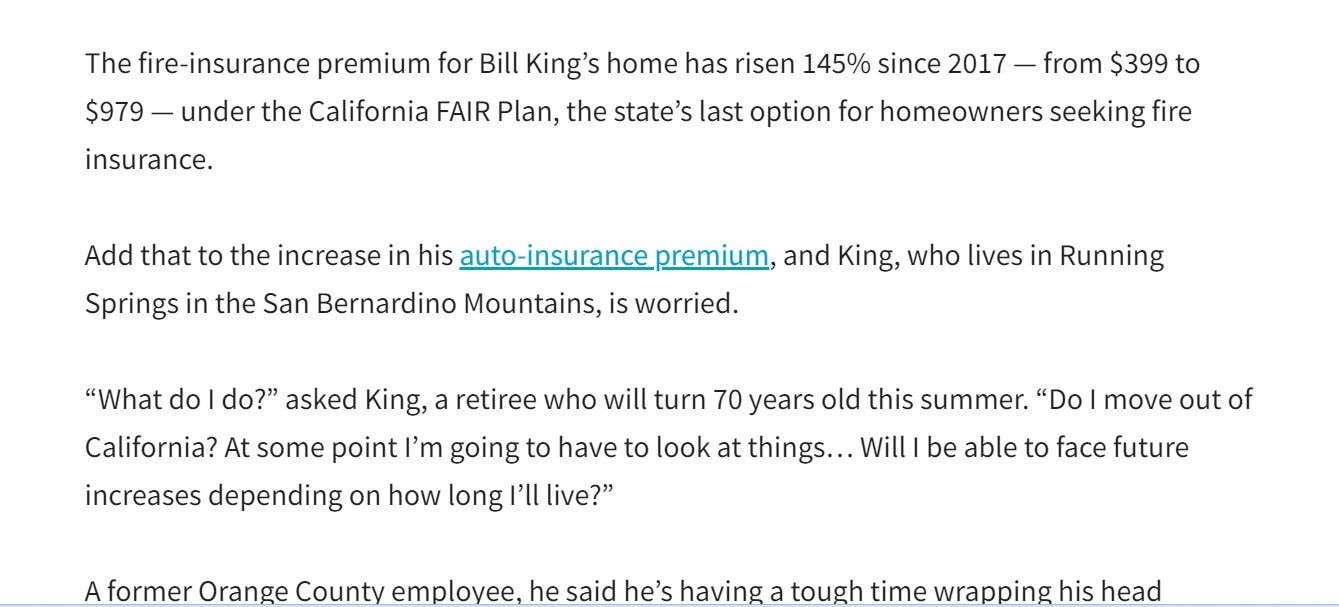

The first idea in real estate investing is “location, location, location”. In some parts of California, wildfire risk is rising and insurers must raise rates in order to be profitable. Incumbent homeowners are pleading poverty. Here is one example from this article.

My economics logic offers the following lessons for Mr. King

#1 Why can’t he tap into his housing equity and pay for market insurance?

#2 Why can’t he sell 50% of his house to a private equity firm? The private equity firm would then insure the asset.

#3 Why can’t he invest in climate fortification to offset fire risk and then choose not to have fire insurance for his home?

#4 Why can’t he sell his home to a private equity firm and sign a lease to live there for the next 10 years?

Of course, he wants to pay $0 to offset the risks but this isn’t realistic.

Note that my microeconomic logic focuses on contract details to share the risks. Note that I didn’t mention government here. The market can handle these risks. Note that the resale value of his home will rise if he takes climate fortification steps.

Mr. King is flipping a two sided coin. Home prices can rise and they can fall. If homeowners are not willing and able to fortify their assets against risks then they should sell them to someone with an edge in doing so. Comparative advantage is an important idea! If private equity firms own more at risk real estate, then we actually face LESS risk because they have the data, skill and access to capital to offset this risk. This is the CLIMATOPOLIS MINDSET!